Overanalyzing our Spotify Wrapped: What MIDiA’s stats say about the industry

Tatiana Cirisano breaks down data from 15 MIDiA staff members to understand what Spotify Wrapped reveals about discovery, listening trends and the business of music.

What Spotify Wrapped reveals

by Tatiana Cirisano from MIDiA Research

Last year, as Spotify’s annual Wrapped series hit the internet, MIDiA did what we do best: analyse, publishing a blog piece on what our own year-end data reflects about the state of music streaming and fandom. Now, we are back for the second annual edition of MIDiA Wrapped, with plenty of new themes to unpack.

These reflections are based on the Wrapped stats of 15 members of the MIDiA team (and, where noted, a handful of friends and family members to help round out the data). Of course, the major caveat is that these are the listening habits of a small number of entertainment analysts, many in younger age demographics, and so are far from representative of the wider population. Also, Wrapped engagement covers 11 months out of the year, excepting the holiday period when listening habits often change notably, at least for those in the Western regions.

Nonetheless, untangling our own data revealed broader learnings for the industry. Below are three major takeaways from the exercise.

1. Our top artists represented only 3-6% of our total listening time

Perhaps the most striking thing about our Wrapped stats this year was just how little listening time our “top” artists account for. The majority (60%) of MIDiA staff fell into the 3% to 6% range for top artist minutes as a percentage of total minutes. There was an average total listening time of 527.6 hours, and an average top artist listening time of 24.2 hours.

This was even the case for MIDiA staffers who were high up in their top artists’ percentiles of listeners. For example, one staff member landed in the top 0.1% of listeners for her favourite artist, yet that artist still accounted for only 7.0% of her total listening.

Fragmentation is the likely culprit here. In the streaming era, consumers are empowered (or algorithmically recommended) to listen to a wider range of songs and artists than ever. This means that the “hits” are less dominant than before. Imagine if we were able to access a Wrapped for our listening in the CD era. It is likely that our top artist back then would account for a greater percentage of total listening (say, 25% or more), given that the average person owned far fewer CDs by a much smaller range of artists than the number of albums, artists, and songs they listen to today.

State of the independent music economyFragmentation and consolidation

This report presents the results of MIDiA’s annual independent label and distributor survey, as well as the most comprehensive market sizing of the non-major label sector ever conducted. Built on revenue…Find out more…

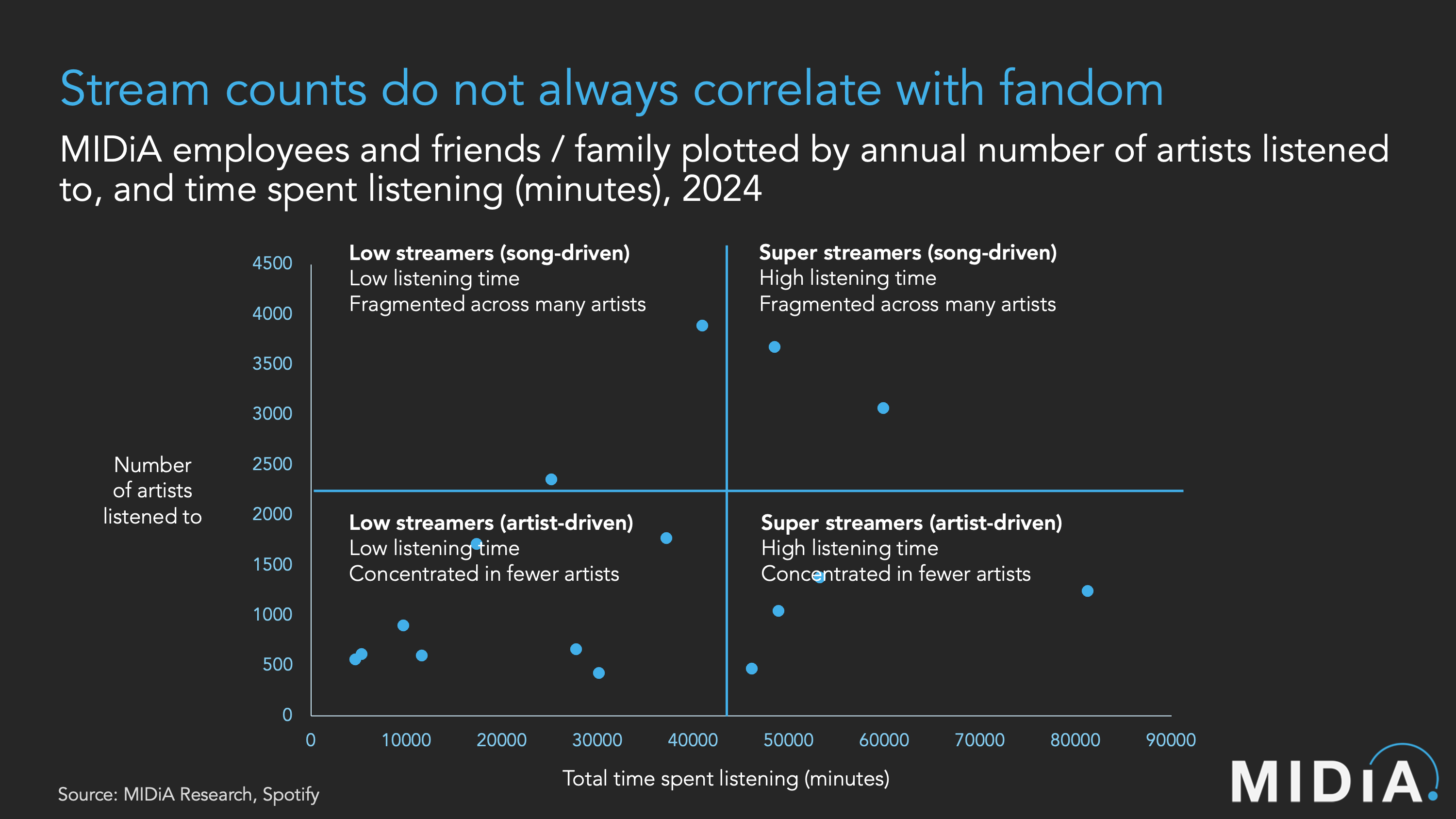

2. Stream counts do not always correlate with fandom

Time spent listening is one way to measure music fandom, but not the only way — and understanding this data requires context. For example, a high number of minutes spent listening could mean an active music fan, but it could also mean a passive listener streaming algorithmic playlists in the background of work all day. Another crucial differentiator is artist-focused listening versus song-focused listening. For example, it makes quite a difference for individual rightsholders whether someone listens to 12 hours of their favourite artist, or 12 hours of songs by 100 different artists.

So, to better contextualise our listening, we next plotted MIDiA staffers (and a handful of friends and family) by total listening time and number of artists listened to. This created four segments:

Purely in terms of streaming payouts, the passive listeners who stream all day would be more valuable than those who concentrate on their favourite artists, but spend less time listening overall. (Of course, more total listening also means the royalty pot gets divided up in more ways.) Yet, in terms of an artist’s longevity and connection to their fans, it is the latter who may be more valuable and who may be more likely to spend more on merch and tickets. The majority of people in our sample fell into this lower-left quadrant and among them are MIDiA’s most fervent music fans.

You can quickly see how the interests of Spotify, labels, and individual artists begin to diverge here. Spotify’s best interest is for users to listen for longer, regardless of what they listen to — but it may be even better for their listening to be more fragmented, such that the user’s strongest relationship on the platform is not with any particular artist, but with Spotify itself. The labels’ best interest is also in those fans who stream the most, but it is better if their listening is less fragmented, as fragmentation is slowly but steadily reducing the ability for superstars to dominate. For artists relying more on merchandise and tickets, it may in fact be the fans who stream less, but focus on artists more, who are the most valuable.

The lesson here is that all types of streaming are not made equal — and in fact, the music industry needs all types of listeners. Each plays a separate role in building artist careers with strong fanbases, longevity, and sustainable income.

3. Streaming’s last cultural moment?

There was a time somewhere around the mid-2010s when cultural moments happened on streaming platforms. Think Spotify’s RapCaviar playlist and the heyday of its Best New Artist Grammys party, Frank Ocean surprise-dropping Blonde exclusively on Apple Music, or Beyoncé doing the same for Lemonade on TIDAL.

Over the 2020s thus far, streaming has steadily lost cultural capital to social, and in particular, social video. Scenes, fandom, and culture happen on social platforms and trickle down to streaming, not the other way around. Spotify’s Wrapped is arguably the last streaming-oriented cultural moment standing. But is Wrapped even a streaming moment when everything about it is designed for social media?

Something else has changed, too. Wrapped has become so co-opted by brands and meme culture that the number of posts riffing on Wrapped seem to eclipse the number of posts that are actually Wrapped. While these sorts of posts might be thought of as free marketing for Spotify, we are at the point where they are competing with Spotify for consumers’ time and attention. A similar trend is developing across entertainment: today’s consumers may spend more time engaging with user-generated content around a brand than with the brand itself. The strongest takeaway from this year’s Wrapped may be that social is where music moments happen — even streaming ones.

Want the latest entertainment research and insights directly to your inbox? Our newsletter has you covered, click here to subscribe.