____________________________

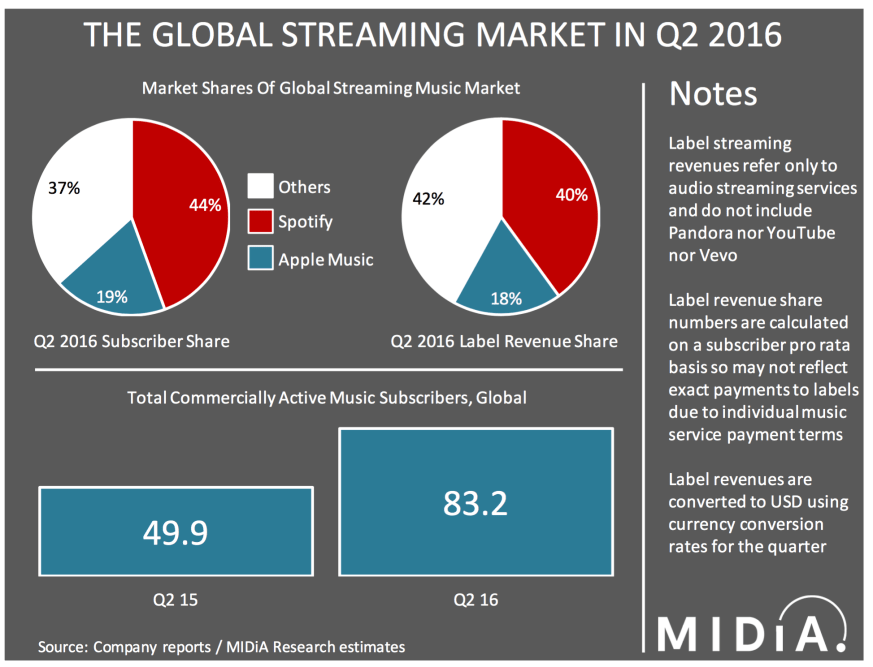

Guest Post by Mark Mulligan on his Music Industry BlogSpotify has just delivered 2 landmark data points: 40 million subscribers and $5 billion paid to rights holders to date. Although the 3 million added in Q3 was down on the 7 million added in Q2 (boosted by a summer pricing promo) there is no escaping the fact that Spotify’s momentum has accelerated rather than declined since the emergence of Apple Music. 2016 is proving to be Spotify’s year. The question is how well the rest of the market is performing beyond the 2 market leaders?The streaming music market as a whole is experiencing unprecedented growth, with the major labels collectively reporting a 52% increase in streaming revenue in Q2 2016 compared to the same period 12 months ago. Given that total streaming revenues (including YouTube etc. but not Pandora) grew by 44% in 2015 (according to the IFPI) the picture that is emerging is one of, at worst, sustained growth, at best, accelerating growth.Although the major label numbers have to be interpreted with caution due to factors such as Minimum Revenue Guarantees (MRGs) – see my previous post for much more detail on this – the headline trend is growth. However, headline growth is not necessarily a reflection of how most of the market is actually performing. In fact, a forensic examination of these numbers cross referenced against reported Apple Music and Spotify numbers reveals that the outlook for the rest of the pack is very different indeed.

Related articles